-1.png?width=1812&height=1072&name=TripAdvisor%20%26%20More%20Bookings%20(1)-1.png)

-2.png?width=1812&height=1072&name=Google%20Bookings%20(1)-2.png)

.webp?width=200&name=Restaurants-Bars-Featured%20(1).webp)

-1.png?width=200&name=TripAdvisor%20%26%20More%20Bookings%20(1)-1.png)

-2.png?width=200&name=Google%20Bookings%20(1)-2.png)

-1.png?width=200&name=Instagram%20Bookings%20(1)-1.png)

-1-png.webp?width=200&name=Facebook%20Integration%20Rectangle%20(1)-1-png.webp)

.webp?width=200&name=download%20(1).webp)

%20(1)-2.webp?width=200&name=Eat%20(34)%20(1)-2.webp)

%20(1)-2.webp?width=200&name=Eat%20(18)%20(1)-2.webp)

Running a restaurant is no easy business. As a restaurant owner, you have to look after and keep track of every aspect of your operations - staff, raw materials, customer service, sales volume, and more. The list goes on and on.

However, oftentimes restaurant owners and managers tend to overlook the most important side of running a business - the financials.

The financial side of running a restaurant can be dull and not as exciting as what’s happening in the kitchen. You would understandably want to spend all your time trying to improve your restaurant’s operations rather than reading a bunch of boring papers. But here’s the thing, these papers are what keep your kitchen running.

Even if a restaurant’s financial accounts are being handled by professional accountants or institutions, it’s important for restaurant owners to be able to read financial statements and have a good understanding of where their restaurant is at, money-wise.

Keeping track of the money business at the restaurant on a regular basis allows owners to understand how well their restaurant is performing and identify any factors that may be significantly affecting revenue in a positive or negative way.

If numbers are not your thing, reading and understanding financial statements can seem like a daunting task. The good news is that you don’t have to be an expert in finance to run a successful restaurant.

Learning how to understand the three main financial statements: income statement, balance sheet, and cash flow statement can help you understand your business’s financial standing.

Together these financial statements provide a holistic view of a restaurant’s performance and help restaurant owners in making informed decisions.

Note

Note: Reviewing restaurant financial statements is crucial for making informed decisions and improving profitability. Work with a professional accountant or bookkeeper for accurate financial reporting.

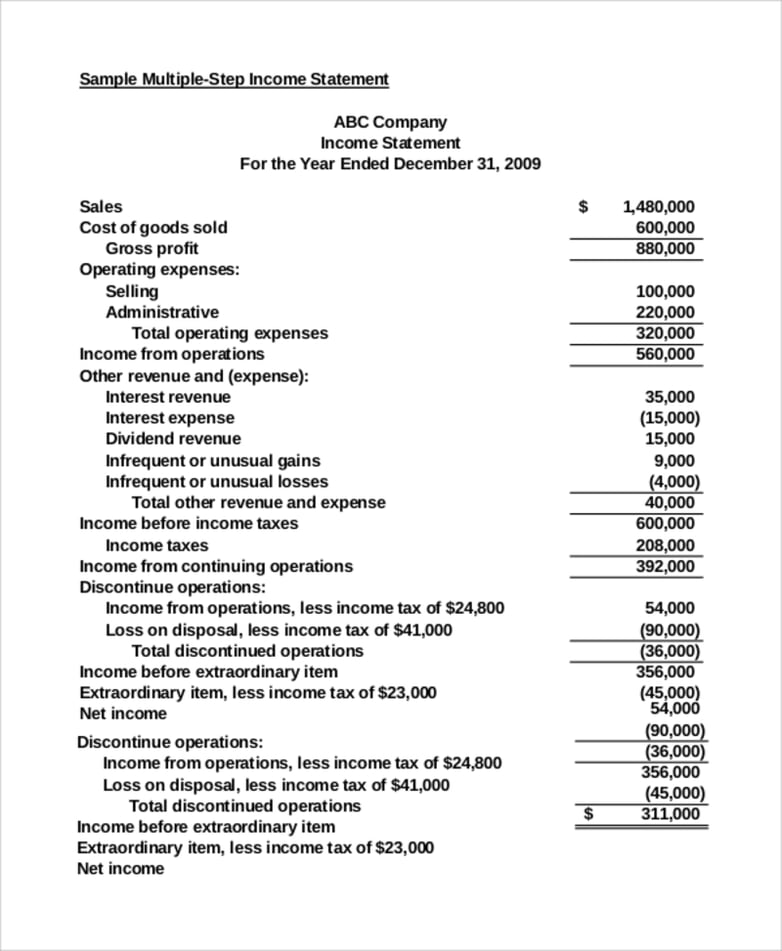

Income vs profit and loss statements

A restaurant’s income statement, also known as the profit and loss (P&L) statement, gives an overview of its expenses and revenue and summarizes its profits or losses for a given period of time. The income statement helps restaurant owners understand how much they have spent, how much they have earned, and how much profit they have made in a certain time frame.

This statement takes into account all the revenues and expenses of a restaurant, like total sales, cost of goods sold (CoGS), prime costs, labor costs, and operational costs while calculating a restaurant’s net profit or loss.

Income statements can be made on a weekly, monthly, quarterly, or yearly basis, with the maximum time frame being 12 months.

Understanding income statements is crucial for restaurant success as it helps restaurant owners:

- Get an in-depth overview of their expenses and what the money is being spent on.

- Get a better understanding of their revenue and know whether the restaurant is running in a profit or loss.

- Compare current financial data with previous years to understand if the restaurant is performing up to the key performance metric standards.

- Identify pain points that may be negatively affecting the restaurant’s profit and take strategic decisions to overcome them. For instance, if restaurant owners notice a significant spike in the CoGS during a quarter, they can find out what caused it (increase in raw material prices, increase in demand, etc), and make decisions to minimize that expenditure.

How to create a restaurant income statement

As mentioned above, the income statement includes all the revenue and expenses of a restaurant. It calculates a restaurant’s net profit or loss for a given time period in the following way:

[Total Sales] - [CoGS] - [Prime Costs] - [Operating Cost] = Net Profit/Loss

Each section is broken down into more parts depending on the restaurant's operations. For instance, total sales would be broken down into food, liquor, events, etc.

Balance sheet

While the income statement does a good job at providing information about the restaurant’s financial happenings over a period of time, it’s not enough on its own to properly understand the restaurant’s performance. An income statement does not include the assets and liabilities owned by a restaurant, and thus, does not provide a complete picture.

A balance sheet helps restaurants get an understanding of a restaurant’s financial position at any given date. It takes into account the restaurant’s assets and liabilities and calculates the restaurant’s equity to know its net worth on that particular date.

How to create a balance sheet

A balance sheet includes:

- Assets: what the restaurant owns of value, including cash, inventory, machinery, property, etc.

- Liabilities: what the restaurant owes to others, like loans, rent, outstanding bills, etc.

- Equity: a restaurant’s life-to-date earnings or loss. Equity is calculated by deducting the restaurant’s liabilities from its assets. A portion of equity includes retained earnings, which is a restaurant’s net income that is reinvested into the business as additional equity capital.

- Annual Report: A comprehensive financial review of your restaurant's performance, providing valuable insights for informed decision-making and regulatory compliance

Cash flow statement

A cash flow statement gives a detailed record of the cash coming in and going out of your restaurant. It keeps track of cash flow related to your restaurant’s fundamental operations like labor cost, supply cost, sale of assets, etc. for a given time period.

It also includes any financing or debt taken up by the restaurant as that can affect the cash flow. For instance, increased debt could mean there is more cash as you have taken a loan from somewhere, and decreased debt can mean less cash as you have paid off a liability.

Keeping track of cash flow statements is crucial for restaurant success as it helps owners better understand exactly where their cash is going and coming from. It also helps restaurant owners forecast future cash flow to ensure that they have sufficient funds to manage and finance the restaurant’s current operations and growth projects.

How to create a cash flow statement

A cash flow statement consists of three main parts:

- Operating activities: These include your revenue-generating activities like net income, sale of assets, etc.

- Investing activities: These include cash transactions that affect assets you have invested in, like equipment, property, marketable securities, etc. Any purchase of assets decreases the cash flow.

- Financing activities: These include debt and equity transactions like paying dividends, borrowing funds, etc. These activities are taken from the balance sheet.

If the cash payments are greater than the cash receipts, then there is a negative cash flow or a cash outflow, which means that your restaurant has spent more cash than it has earned.

If the cash receipts are greater than the payments, then there is a positive cash flow, which means that your restaurant has earned more money than it has spent.

Tips to understand a restaurant’s financial performance

While having a good understanding of these three financial statements is fundamental for keeping track of your restaurant’s performance, it’s also important to know what’s happening at your restaurant on a daily basis and double-click on your restaurant’s performance to always stay informed.

How many people are visiting your restaurant on a daily basis? How many customers are returning to your restaurant? What days and times does your restaurant get the most diners? What does the average guest spend? These are all important factors that should be analyzed on a regular basis to have a good understanding of your restaurant's performance.

As a restaurant owner who has multiple things to do, it can get difficult to keep track of all these metrics. It’s nearly impossible to manually collect and analyze this data on a regular basis. Thankfully, technologies like table management systems now exist to help restaurant owners do just that.

Eat App’s advanced reporting system, for instance, collects in-depth guest data including preferences, average guest spend, busiest time periods, new vs. returning customers, etc. that provides restaurant owners with an in-depth insight into their restaurant’s performance and helps them make informed decisions.

You can also get deeper financial insights from your POS by integrating your POS system with Eat App. This opens up a plethora of data regarding spending habits, previous orders, etc. that helps restaurants make more informed and accurate predictions about future sales and cash flow.

Want to try Eat App’s reporting feature for your restaurant? Get started with your free 14-day trial now.

%20(1)-1.webp?width=314&height=175&name=Eat%20(62)%20(1)-1.webp)

.webp?width=144&height=72&name=Eat%20App%20Logo%20(3).webp "Eat App")